It’s Not Too Late to Save for Retirement in Your 50s

So you are in your 50s and still have a good distance before you hit the minimum retirement age in Singapore, which is set to be 65 years in 2030. Until that happens, life is good. You’re at the peak of your career, earning a decent salary and living the life you’ve built for yourself. But what happens after you retire? Would you have enough to sustain your lifestyle for the next twenty years after?

After all, household expenditures have been increasing over the years. According to the Household Expenditure Survey released in 2019 by the Department of Statistics Singapore, the average household spent between $2,570 to $7,573 per month, depending on their income bracket. With inflation and the rising cost of healthcare, these figures are likely to be higher by the time you retire.

Even though your expenses are likely to be halved during retirement, it’s still no chump change. To sustain your lifestyle, it’s important that you have enough savings set aside for your expenses. Or even more. After all, retirement these days isn’t just about meeting your basic needs. Instead, it’s having the freedom to pursue your dreams and making meaningful relationships.

Think about where you are in your retirement planning. Do you have enough in your funds to lead your desired lifestyle post-retirement? If you don’t, it’s still not too late to play catch-up. Here are some of the best ways to save for retirement in your 50s.

1. Contribute more to your CPF

With CPF, you can enjoy high, (pretty) low-risk interest on your savings. Capitalise on the high interest rates of 2.5% p.a. and 4% p.a. in your Ordinary Account (OA) and Special Account respectively. The government also pays an extra 1% p.a. interest on your combined balances, or if you’re above 55 years old, an additional interest of up to 2% p.a.!

Although you can start withdrawing your CPF funds once you turn 55, avoid withdrawing them unless it’s truly necessary. In this low-interest climate, the interest rates for your CPF accounts are much higher than what’s available at the banks.

You can also make voluntary contributions (VC) to get the most out of the CPF rates. When you turn 50 years old, your personal contribution rates for your Special Account (SA) and Ordinary Account (OA) will automatically be reduced, and even more after you turn 55.

However, you can choose to maintain your prior contribution rates by making a VC. This way, you’ll be earning more interest than you would if you were to put your cash into a bank account. Do note that there is a cap for VC – it’s the difference between the CPF Annual Limit and the amount of mandatory contributions (MC) made for the calendar year. Excess VC will be refunded without interest.

If you are between 55 to 70 and have yet to meet the Basic Retirement Sum in your Retirement Account (RA), here’s another reason to make a VC. Under the Matched Retirement Savings Scheme (MRSS) launched in 2021, the government will match cash top-ups made to your RA, capped at $600 per year over five years. Find out if you are eligible for MRSS here.

As an added bonus, you get to enjoy tax reliefs of up to $14,000 per calendar year whenever you make cash top-ups to your CPF accounts or your loved ones’. This comprises a tax relief of up to $7,000 if you are topping up for yourself and an additional $7,000 if you are topping up for your parents, spouse or siblings. Don’t underestimate the savings you can get out of this; the 50s are your peak earning years and taxes can be sizable.

And if you need another reason to continue working, the CPF contribution rates for workers aged 55 to 70 years will also be raised to help Singaporeans save more for their retirement. This increase will go directly to your SA for a larger boost to your retirement income.

Besides working contributions or cash top-ups, another way to get more out of your CPF savings is to delay your CPF LIFE payouts. You can start your CPF LIFE payouts anytime between 65 to 70 years of age, but for each year of delay, your payouts will increase by up to 7% thanks to the CPF interest rates.

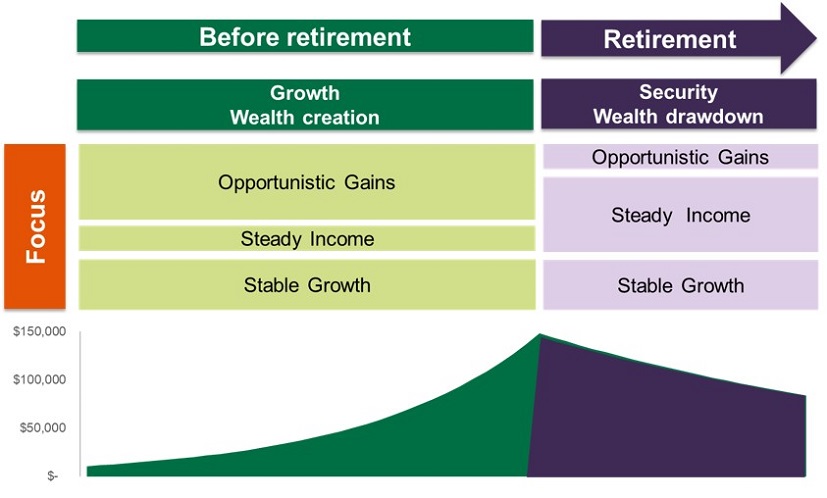

2. Relook your investments and focus on growing wealth

There is no one-size-fits-all solution when it comes to investing but the general rule of thumb is to invest according to your life stage and objectives. For instance, you should focus on growth and wealth creation before you retire. Once you retire, your priority should be stability and generating a steady income.

High yields usually come with higher risks. This is an approach you can afford to take when you are younger as you’ll have a longer investment horizon to remedy things and recover should things go awry. But as you grow older, the more prudent approach is to focus on safe and stable growth, so you don’t erode the savings you’ve built up over the years.

Look into diversifying your portfolio and review it on a regular basis. Adjust it accordingly to achieve your desired rates of return at a risk level that is acceptable to you. If you are looking for greater stability, consider balancing your exposure between both safe and riskier types of asset groups. Safer investments include the likes of CPF, bonds and insurance savings plans.

One example of an insurance savings plan that lets you enjoy a steady stream of income when you retire is Income's Gro Retire Flex Pro. Other than the flexibility to choose when you want to start receiving your monthly cash payouts1, you can also opt to accumulate your cash payouts1 at an interest rate of up to 3.00% p.a.2.

On the other hand, products such as Investment-Linked Plans (ILPs) and Exchange Traded Funds (ETFs) hold relatively more risk.

If you’re on track to meeting your retirement needs and have extra cash to spare, you could consider channeling them to lower-risk products such as single premium insurance savings plans. These are generally safer than volatile options like stocks, and are an alternative if you want to get more out of your savings.

However, if you find yourself still some distance away from reaching your retirement goals, you may have to take slightly more aggressive steps in the next few years to close the gap. If you are not confident of investing on your own, consider getting a financial advisor to help review your portfolio and identify ways to achieve your retirement goals sustainably, at a risk level that you’re comfortable with.

Before purchasing a financial product, always make sure you read up and understand its risks, suitability and terms and conditions. You can also check the credibility of the provider of a financial product at ACRA and Investor Alert List on the Monetary Authority of Singapore's website.

3. Delay retirement

Hitting the retirement age doesn't mean you have to retire. If you enjoy your job, can and want to continue working for a few more years, why not? You'll be able to fill your time and continue building your nest egg for an even more comfortable retirement lifestyle when you’re ready.

Singapore will be raising the minimum retirement age and re-employment age gradually to 65 and 70 years respectively by 2030. By default, that means you will be able to work for a longer period. Instead of retiring at the minimum retirement age, consider delaying it by opting for re-employment, especially if you need more time to fill the gaps in your retirement plan.

Under the Retirement and Re-employment Act (RRA), companies are obliged to offer eligible employees up to five more years of work once they hit the minimum retirement age. Otherwise known as re-employment, eligible employees who are medically fit and perform satisfactorily at work may be renewed on a contract basis, which can be anything between one to five years.

However, re-employment is not guaranteed and depends on your work performance each year. Your responsibilities and salary may also change when you get re-employed. For greater employment stability, be ready to adapt and take on new responsibilities. Continue to upskill yourself and attend training to keep yourself relevant. Be open to learning new things and make use of your SkillsFuture credits to pick up skills relevant to your role or industry.

At the same time, consider additional income revenues for greater financial stability. Play to your strengths and opportunities around you and develop a side hustle. This could include speaking engagements, consulting or providing training if you are an expert in your field, starting your own home-based business, or even doing deliveries in your free time.

By earning more income - whether it is through extended employment or a side hustle - you have a longer runway for saving and investing, which ultimately leads to higher returns and a more comfortable retirement.

Plan for your retirement as soon as possible

While it is never too late to start planning for your retirement, the earlier you start, the more time you have to put your plan into action. With a longer investment horizon, you can also afford to take more risks and re-invest your returns to create more wealth and build the retirement life that you’ve dreamed of.

Take some time to figure out what’s the best way for you to save for retirement in your 50s. If you are looking to expand your portfolio, find out how these savings and investment plans can help you reach your retirement goals, or consult our Income advisors if you need help getting started on your retirement plan.

1 The cash payout consists of a monthly cash benefit and a non-guaranteed cash bonus.

2 Interest rate of 3.00% per annum is not guaranteed. Prevailing interest rate at the point of deposit will be determined by us. Any cash benefits paid under the Disability Care Benefit cannot be accumulated with us.

This article is meant purely for informational purposes and does not constitute an offer, recommendation, solicitation or advise to buy or sell any product(s). It should not be relied upon as financial advice. The precise terms, conditions and exclusions of any Income Insurance products mentioned are specified in their respective policy contracts. Please seek independent financial advice before making any decision.

These policies are protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact Income Insurance or visit the GIA/LIA or SDIC websites (www.gia.org.sg or www.lia.org.sg or www.sdic.org.sg).

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Related Articles