Announcement

(I) Benefit changes to IncomeShield Standard Plan (ISIP)

From 1 April 2026, upon renewal of an ISIP policy, there will be three benefit changes.

i) <REVISED> Coverage for Cell, Tissue and Gene Therapy (CTGTP) under Normal Ward

The Ministry of Health (MOH) has expanded MediShield Life coverage to high-cost treatments, including CTGTP, that are clinically and cost-effective. To align with MOH’s guidelines, your policy will only cover CTGTP treatments that are specified on MOH’s CTGTP List (go.gov.sg/ctgtp-list).

ii) <REVISED> Coverage for High Cost Drugs under Normal Ward

MediShield Life has expanded its coverage for high-cost drugs for blood conditions and conditions with childhood onset. You can refer to MOH’s website at go.gov.sg/mshlbenefits for the list of these high-cost drugs. To align with MOH’s guidelines, your policy will only cover High Cost Drugs that are specified on MOH’s list.

iii) <UPDATE> Coverage for MIC@Home

Mobile Inpatient Care @ Home (MIC@Home) is an alternative inpatient care delivery model that offers clinically-suitable patients the option of being hospitalised in their own homes, instead of a hospital ward. This benefit has been in place since 1 April 2024 and it will now be reflected in your policy conditions.

Please refer to the policy conditions for further details.

(II) Updates on Deluxe Care, Plus, Classic Care and Assist rider

As Deluxe Care rider and Classic Care rider do not meet MOH’s new requirements for Integrated Shield Plan (IP) riders, both riders will be withdrawn from 1 April 2026 onwards.

Policyholders will not be allowed to purchase the Deluxe Care rider or Classic Care rider from 1 April 2026. Existing policyholders of Deluxe Care rider will not be allowed to downgrade their rider to Classic Care rider, and those on Classic Care rider will not be allowed to upgrade to Deluxe Care rider.

If policyholders had bought a Deluxe Care, Plus, Classic Care or Assist rider before 27 November 2025, MOH’s new requirements for IP riders will not apply to the existing rider for now. At this juncture, the existing rider will continue to cover the IP main plan’s deductible and the co-payment limit remains at $3,000 in each policy year.

If the purchase of the Deluxe Care or Classic Care rider is between 27 November 2025 and 31 March 2026 (both dates inclusive), MOH’s new requirements for IP riders will apply to the Deluxe Care or Classic Care rider no later than the next policy renewal after 1 April 2028. More information will be shared with these policyholders in due course.

As part of our regular review of our IP plans and IP riders, we will continue to assess if changes will be needed to keep healthcare insurance sustainable for our policyholders. Like always, we will keep our policyholders informed of policy changes, if any.

(III) Welcome discount for IncomeShield Standard Plan (for new applications only)

Welcome Discount is a one-time 15% discount on the first-year premium for new policy applications – between 1 April 2026 and 31 March 2027 (both dates inclusive)– for IncomeShield Standard Plan, if there is no additional exclusions or premium loading applied to the policy upon policy issuance.

The Welcome Discount will be applied to the premium payable for the additional private insurance coverage portion of the main plan. The Welcome Discount does not apply to the MediShield Life (MSHL) portion of the main plan. Other promotion terms and conditions apply.

Click here for the full Welcome Discount terms and conditions.

For more information on the changes, please read our FAQs here.

The Ministry of Health (MOH) has introduced new design requirements for Integrated Shield Plan (IP) riders that are made available for sale from 1 April 2026 onwards, as per their announcement on 26 November 2025.

The new requirements are:

i) No coverage for minimum IP deductible – IP riders will not cover the main plan’s minimum deductible.

ii) Higher co-payment cap – the minimum co-payment cap of IP riders will increase from $3,000 to $6,000 in each policy year.

The co-payment cap will also exclude the IP main plan’s minimum deductible.

For more details on the new requirements for IP riders, you can refer to MOH’s announcement at go.gov.sg/ipriderchanges2025.

For new customers

If you were to buy a Deluxe Care or Classic Care rider from 27 November 2025 to 31 March 2026 (both dates inclusive), the new requirements will apply to your Deluxe Care or Classic Care rider no later than your next policy renewal after 1 April 2028.

For existing customers

If you had bought a Deluxe Care, Plus, Classic Care or Assist rider before 27 November 2025, the new requirements will not apply to your existing rider for now. As part of our regular review of our IP plans and IP riders, we will continue to assess if changes will be needed to keep healthcare insurance sustainable for our policyholders. Like always, we will keep our policyholders informed of policy changes, if any.

For more details on the impact of the new requirements to Income’s IP riders, please read our FAQs here.

Should you have further queries, we would be most happy to assist you via your preferred mode of contact at income.com.sg/contact-us.

We are continuously making efforts to ensure our plans remain affordable and sustainable for our policyholders while catering to their healthcare needs.

In the recent few years, the industry has implemented various initiatives to balance healthcare coverage, encourage prudent consumption of healthcare services, and enable health insurance premiums to be more sustainable. These industry initiatives, together with our efforts to extend coverage, form the basis of our premium adjustments and have enabled us to better moderate and reduce premiums where possible in the last few years.

We also remain conscientious in our approach and currently do not subject our customers to higher individual premiums when they make a claim.

The premium adjustments, which differ across age bands, apply to all IncomeShield plans and riders from 1 October 2025, upon renewal of the policy.

Did you know

.webp?language=en "ISIP-did-you-know (1)")

Enhance your MediShield Life coverage with IncomeShield Standard Plan

Up to $200,000 limit in each policy year for medical treatment.

So your loved ones are relieved of the financial burden if something unforeseen happens.

For the insured receiving treatment for multiple primary cancers under the Cancer Drug Treatment Benefit[5] and Cancer Drug Services Benefit[6].

You can use MediSave to pay your premiums (up to the Additional Withdrawal Limits[7]).

For a more detailed look at what you are covered for, you may view the full coverage table here.

Seek medical care through our panel of trusted medical professionals

Access to our panels[8] of over 600 specialists across various specialties and sub-specialties in private practice island-wide, specially curated to meet your medical needs at quality clinical standards.

For withdrawn riders (Deluxe Care Rider, Classic Care Rider, Plus Rider, Assist Rider, Daily Cash Rider and Child Illness Rider), read more here.

What our customers have said about us

Your policy toolkit

Eligibility and payment frequency

There is no maximum entry age limit for IncomeShield Standard Plan.

You need to make payment every year.

View full premium table for Main Plan

You may refer to MOH’s website for a comparison of Integrated Shield Plans (IPs) across all insurers, including the estimated premiums you have to pay for an IP over your lifetime.

Learn more about the drivers of premium here.

Policy conditions

Your queries answered

IncomeShield Standard Plan is Income Insurance’s offering for Standard Integrated Shield Plan (Standard IP).

Integrated Shield Plans (IPs) comprise two components – the MediShield Life component and additional private insurance coverage. Those covered under IPs enjoy the combined benefits of (i) MediShield Life, run by the Central Provident Fund (CPF) Board, and (ii) the additional private insurance coverage for Class A/B1 and private hospital stays, run by private insurers. IncomeShield is Income Insurance’s offering for IP.

The Ministry of Health has worked with private insurers who offer IPs, including Income Insurance, to develop Standard IP to offer affordable coverage with similar benefits across all IP insurers for Class B1 wards. MediShield Life provides coverage for Class B2 and C wards only.

Benefits of Standard IP are standardised across all IP insurers. However, there will be variances in the premiums of Standard IPs offered by different IP insurers as each insurer takes into account the company’s estimation of claims and expenses, risk management policies and other relevant factors.

In designing the Standard IP, it was important to balance between providing adequate coverage and ensuring premiums remain affordable. The Standard IP was thus intended to be a “no-frills”, affordable product targeted at large hospital bills and selected costly outpatient treatments.

MediShield Life is able to cover pre-existing conditions because the cost of providing such coverage is shared among those with pre-existing conditions, the community and the government, which bears the bulk of the costs (about 75%). Unlike MediShield Life, private insurers are unable to provide cover for pre-existing conditions. Hence, these pre-existing conditions will be excluded from the additional private insurance coverage portion under your IncomeShield Standard Plan.

If you are a Singapore Citizen and Permanent Resident, you will continue to be covered by MediShield Life even if you are covered under IncomeShield Standard Plan. This means that you will be enjoying the combined benefits of (i) MediShield Life, run by the Central Provident Fund (CPF) Board, and (ii) the additional private insurance coverage by Income Insurance for Class B1 hospital stay.

No, you can only be insured under one Integrated Shield Plan at any point in time. Your current Integrated Shield Plan will be automatically terminated upon commencement of a new Integrated Shield Plan.

Income Insurance will apply its own guidelines on the assessment of risks. If you have any additional information about your health, you may give this to us for a review of our earlier decision.

Deductible means the part of the benefit you are claiming that the insured must pay before we will pay any benefit. The deductible is shown in the schedule of benefits. Co-insurance means the amount that you need to pay after the deductible. The co-insurance percentages for the benefits are shown in the schedule of benefits. Co-insurance applies to all claims made under your policy except for final expenses benefit.

No, IncomeShield Standard Plan is guaranteed renewable for a lifetime. This means that after you have been accepted, any change to your health status does not affect your current insurance coverage.

You can access our health coverage tool here to find out if your treatment is covered under your plan and get helpful information you need to file your claims. All claims submitted are subjected to review in accordance with the terms and conditions of the policies.

You will not be able to purchase any rider as there are no rider options for the IncomeShield Standard Plan.

For existing IncomeShield policyholders, you can choose to upgrade your plan to enjoy better benefit by submitting an upgrade request via My Income customer portal or you can speak to your advisor.

You will need to meet the entry requirements (e.g. maximum entry age) of the plan you wish to upgrade to. Any upgrade of plans will require underwriting.

Your existing Optima Care / Essential Care / Deluxe Care / Classic Care / Plus / Assist rider will have to be terminated as there are no rider options for the IncomeShield Standard Plan. Any unused premiums from the terminated rider will be refunded to you.

No, upon approval of your upgrade application, we will issue you a new policy contract. The change will take effect on the start date indicated on your policy contract.

No, you will continue to enjoy cover up to the benefit limits of your previous plan for these medical conditions. For your upgraded plan, you will be covered for any other medical conditions that you are not excluded from.

Upon a request to upgrade your plan, the current policy will be terminated and a new set of policy document will be issued to you. Any unused premiums from the terminated policy will be refunded to you.

We are using the same policy number for your new plan as it is essentially a conversion or upgrade of plan. This will make it easier for you to remember your policy number.

If you wish to upgrade to a higher plan after your first upgrade, you can do so after 40 days from the start date of your upgraded plan.

Yes, you can. However, you should note that re-application will be subject to Income Insurance’s underwriting and acceptance.

Each insured person is issued an individual insurance policy. Therefore, each upgrade is processed independently and may result in a time difference when receiving your policy contracts.

If you are a Singapore Citizen or Permanent Resident, even though you have terminated your Enhanced IncomeShield/IncomeShield/IncomeShield Standard Plan, you will continue to be covered under MediShield Life.

We would like to highlight that by terminating your Enhanced IncomeShield/IncomeShield/IncomeShield Standard Plan, you will need to re-apply if you wish to be covered in the future. The acceptance of your new application will be subject to Income Insurance’s underwriting and acceptance. Before you terminate the cover, we hope that you will reconsider your decision as it is important for you to have medical insurance coverage to help defray part of the large medical bills in the event of a serious illness or prolonged hospitalisation.

Anyone who pays for, or is insured under IncomeShield Standard Plan is not eligible for Additional Premium Support (APS) from the Government. ^

If you are currently receiving APS to pay for your MediShield Life and/or CareShield Life premiums, and you choose to be insured under IncomeShield Standard Plan, you will stop receiving APS. This applies even if you are not the person paying for IncomeShield Standard Plan. In addition, if you choose to be insured under IncomeShield Standard Plan, the person paying for IncomeShield Standard Plan will stop receiving APS, if he or she is currently receiving APS.

^ APS is for families who need assistance with MediShield Life and/or CareShield Life premiums, even after receiving premium subsidies and making use of MediSave to pay for these premiums.

You may submit your claims via My Income customer portal (me.income.com.sg). For more information on our claim process and other channels to submit your claims, find out more here.

Your re-application for Enhanced IncomeShield/IncomeShield/IncomeShield Standard Plan will be subject to Income Insurance’s underwriting and acceptance. Depending on the underwriting assessment, your application may be:

- Accepted at standard terms

- Accepted with exclusions on any pre-existing medical conditions

- Postponed or Declined

Understand the details

#Based on a survey by Nielsen IQ between January 2023 to December 2025, with 11,040 health insurance policyholders between 21 and 65 years old, Income Insurance ranked first at 33% as a health insurance company that can be trusted in good and bad times.

*We offer 15% off (“Welcome Discount”) on your first-year premium with the purchase of IncomeShield Standard Plan (“Qualifying Policy”). The Welcome Discount is only applicable if no additional exclusion or premium loading is applied to the Qualifying Policy upon policy issuance. The Welcome Discount does not apply to the premium for the MediShield Life portion. Welcome Discount terms and conditions apply. Please refer to income.com.sg/integrated-shield-plan/welcome-discount-tnc.pdf for further details.

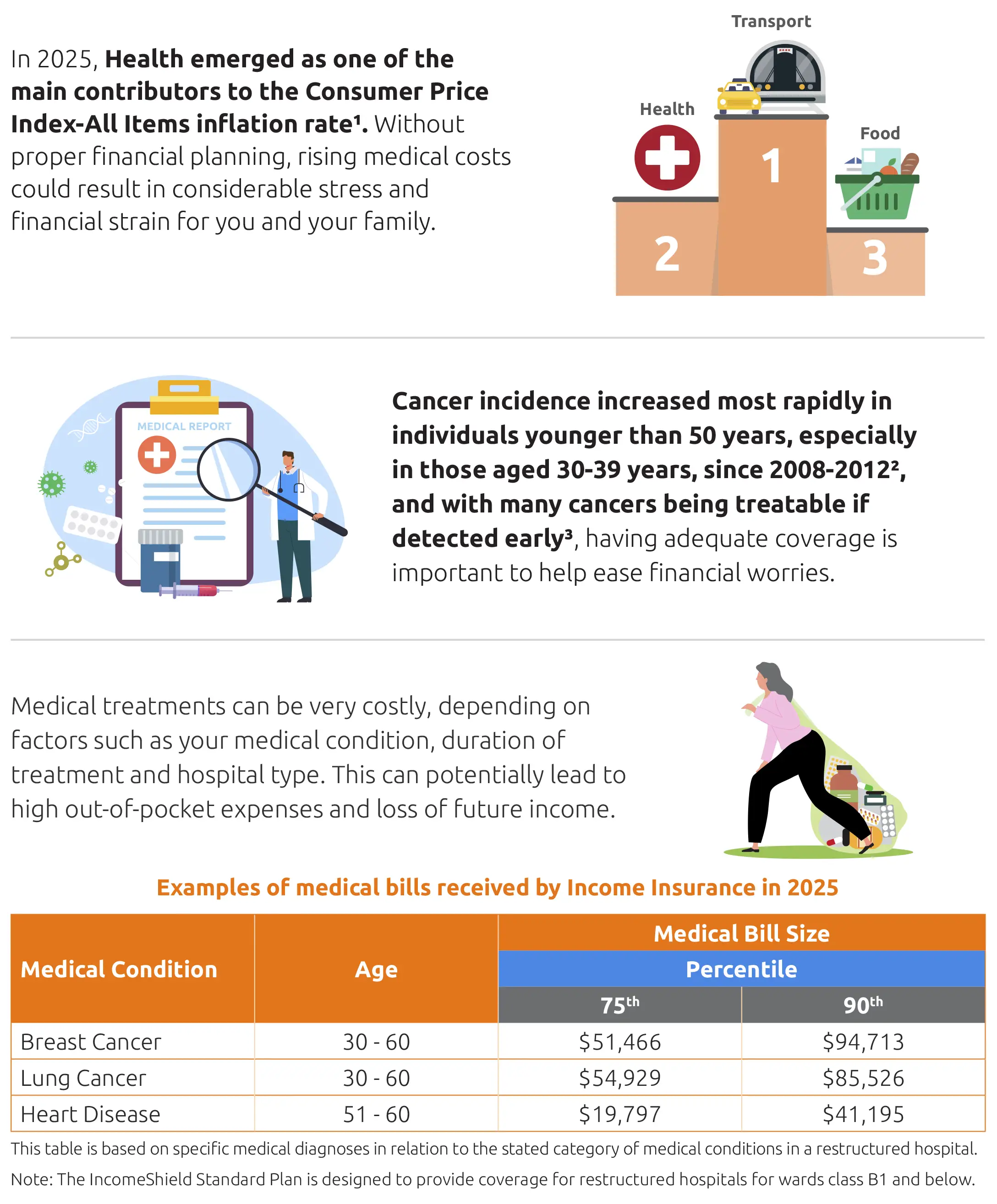

[1]Singapore Department of Statistics, Singapore Consumer Price Index (CPI).

[2]National Registry of Diseases Office, Singapore Cancer Registry Infographic 2022.

[3]National Registry of Diseases Office, Singapore Cancer Registry 50th Anniversary Monograph 1968-2017.

[4]Subject to policy year limits and any benefit limits.

[5]This benefit covers the main outpatient hospital treatment received by the insured from a hospital or a licensed medical centre or clinic. For cancer drug treatment, only cancer drug treatments listed on the Cancer Drug List (CDL) and used according to the indications for the cancer drugs, as specified in the CDL on Ministry of Health (MOH) website (go.gov.sg/moh-cancerdruglist) will be covered. For each primary cancer, if the cancer drug treatment on the CDL involves more than one drug, we allow a particular drug to be removed from the treatment or replaced with another drug on the CDL that has the indication ‘for cancer treatment’, only if this is due to intolerance or contraindications (for example, allergic reactions). In such cases, the claim limit of the original cancer drug treatment on the CDL will apply.

For each primary cancer, if more than one cancer drug treatment is administered in a month, the following will apply.

- If any of the cancer drug treatments that are on the CDL has an indication that states ‘monotherapy’, only the treatments on the CDL that have the indication ‘for cancer treatment’ will be covered in that month.

- If none of the cancer drug treatments that are on the CDL has an indication that states ‘monotherapy’:

- if more than one of the cancer drug treatments administered in a month has an indication other than ‘for cancer treatment’, only cancer drug treatments that are on the CDL and have the indication ‘for cancer treatment’ will be covered in that month; and

- if one or none of the cancer drug treatments administered in a month has an indication other than ‘for cancer treatment’, all cancer drug treatments that are on the CDL will be covered in that month.

Cancer drug treatments not on the CDL will be considered as having an indication other than ‘for cancer treatment’.

For insured receiving treatment for one primary cancer, we will pay up to the highest limit among the covered cancer drug treatments on the CDL that are administered in that month.

The cancer drug treatment on the CDL benefit limit is based on a multiple of the MSHL Limit for the specific cancer drug treatment. For the latest MSHL Limit, refer to the CDL on MOH’s website under “MediShield Life Claim Limit per month” (go.gov.sg/moh-cancerdruglist). MOH may update this from time to time. The revised list will be applicable to the cancer drug treatment which occurred on and from the effective date of the revised list.

The deductible does not apply to the outpatient hospital treatment benefits.

[6]For cancer drug services, it covers services that are part of any outpatient cancer drug treatment, such as consultations, scans, lab investigations, preparing and administering the cancer drug, supportive-care drugs and blood transfusions. It does not cover services provided before the insured is diagnosed with cancer or after the cancer drug treatment has ended.

The cancer drug services benefit limit is based on a multiple of the MSHL Limit for cancer drug services. For the latest MSHL Limit for cancer drug services, refer to “Cancer Drug Services” under the MSHL benefits on MOH’s website (go.gov.sg/mshlbenefits). MOH may update this from time to time. The revised limit will be applicable to the cancer drug services incurred within the policy year of the revised limit.

[7]The Additional Withdrawal Limit (AWL) is the maximum MediSave limit that you can use for your IncomeShield Standard Plan’s additional private insurance coverage premiums. Please refer to moh.gov.sg/healthcare-schemes-subsidies/medishield-life for the latest AWL.

[8]Panel or preferred partner means a registered medical practitioner, specialist, hospital or medical institution approved by us. Our list of approved panels also includes all restructured hospitals, community hospitals and voluntary welfare organisations (VWO) dialysis centres. The lists of approved panels and preferred partners, which we may update from time to time, can be found at income.com.sg/specialist-panel.

There are certain conditions whereby the benefits under this plan will not be payable. You can refer to your policy conditions for the precise terms, conditions and exclusions of the plan. The policy conditions will be issued when your application is accepted.

IncomeShield Standard Plan is available as a MediSave-approved Integrated Shield Plan for the insured who is a Singapore Citizen or a Singapore Permanent Resident. This applies as long as the insured meets the eligibility conditions under MediShield Life. If the insured is a foreigner who has an eligible valid pass with a foreign identification number (FIN), IncomeShield Standard Plan is not available as an Integrated Shield Plan.

This is for general information only and does not constitute an offer, recommendation, solicitation, or advice to buy or sell any product(s). You can find the usual terms, conditions and exclusions of IncomeShield Standard Plan here. All our products are developed to benefit our customers but not all may be suitable for your specific needs. If you are unsure if this product is suitable for you, we strongly encourage you to speak to a qualified insurance advisor. Otherwise, you may end up buying a product that does not meet your expectations or needs. As a result, you may not be able to afford the premiums or get the insurance protection you want. If you find that this policy is not suitable after purchasing it, you may terminate it within the free-look period and obtain a refund of the premiums paid.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact Income Insurance or visit the GIA/LIA or SDIC websites (www.gia.org.sg or www.lia.org.sg or www.sdic.org.sg).

Protected by copyright and owned by Income Insurance Limited.

Information is correct as at 20 July 2026 (SGT).

Learn more about health insurance

Whether it’s for you or your loved ones, know your elderly care options so you can make informed decisions when the time comes.

An all-you-need-to-know guide to health screenings and why you should prioritise it.

Protect yourself from rising healthcare costs & inflation with Integrated Shield Plans. Get enhanced coverage & higher claim limits while securing your finances for the future.